As a SME (small to mid-size enterprise) business leader, you’d certainly like these things; but you are working within a SME budget. You’d also love to be a voice in your community and show your corporate responsibility by supporting environmental sustainability; but, given your SME budget, you never felt this was attainable. However, the market is demanding companies become certified sustainable, and rewarding them for it. Becoming certified is not only affordable and synergistic with your goals and budget, but your growth can be accelerated by it.

Your company can enjoy improved brand image, performance, sales, profit, and valuation; while also supporting your community and the environment via the Edenark Group ISO 14001 sustainability certification program. This is the world’s premier sustainability standard, in +170 countries. We are published by the United Nations. We offer you the best business sustainability certification program, with revenue-enhancement and employee-enhancement benefits, at a price designed for SMEs.

For organizations that care about the environment and future generations…

….and want to be part of a globally-respected solution

….and lead by example

….and be a voice

….and enhance their brand

….and benefit from reduced costs

….and differentiate from competitors; positively impacting revenues

….and help employees be happier, healthier and more productive

Presenter

David Goodman, CEO

David Goodman created and leads Edenark Group. David believes that integrating People, Planet, Promotion and Profit, as a combination, is the only way to maximize a business’ performance and long term value.

David holds a MBA in Finance, Marketing and International Business from Indiana University. He has served as Chairman, Director or CEO of multiple private and public companies. He started his career in the advertising and marketing industries, serving companies like Kraft, Heinz, Keebler, Kimberly Clark, Salada Tea, Pillsbury and Green Giant.

Edenark Group uniquely delivers the world’s premier sustainability certification program, the Edenark Group ISO 14001; providing corporate differentiation and enhancement, improved brand image, sales/revenue/valuation gains, cost reduction, employee wellness/performance enhancement, and overall client organizational improvement.

Moderators

Louis Clovis

CEO-EmpireBay

Green Project Manager

Louis has been in the business for the past 35 years, serving as Sales Director, MD and CEO with a demonstrated history in the Broadcast Sales, Media Production & Events industry. He founded the TV Channel in Sustainability called ESG TV (Environment Social Governance TV) – creating a platform for all NGOs and stakeholders to voice their sustainability concerns world-wide.

He also founded the ReGenAsia Conferences & Workshops and recently became certified Green Project Manager practising the P5 methods in Sustainability.

Tim Worthington

CEO -Zureli Green

Zureli Green Directory

Tim has spent 30 years working across the USA, Europe and Asia and now is the CEO of Zureli one of the world’s largest databases for sustainable products and services.

Zureli offers a free listing for companies that are helping to address climate change as well as several other services that promote their adoption working with both buyers and suppliers of green solutions.

WHAT WE KNOW

88% of consumers (B2C/B2B) want you to be certified sustainable

71% of consumers will move their business to a certified sustainable company

This translates to +$2 Trillion in low hanging fruit

+80% of consumers disbelieve a company that self-certifies

+80% of consumers believe a company that is certified via a globally-recognized standard

WHAT THIS MEANS?

CERTIFIED SUSTAINABLE COMPANIES

…are growing 7.1x faster than their non-certified peers

…deliver a +67% premium to investors versus non-certified peers

…generate +10% sales growth versus non-certified peers

…enjoy +24% Net Income…

…enjoy +11% EBITDA premiums…

…and 4.8% annual stock premiums versus non-certified peers

Should your company be considering sustainability certification?

If so, what should you want from a sustainability certification program?

Is it a passing fad or a long-term global requirement?

Is it a “feel good” project, a “profit-driving” project, or both?

Will it be hard for your organization to implement?

How long will it take to start seeing promotional value?

What are the odds of seeing operating cost/carbon savings?

Will it have a positive impact on your brand?

Will it give you a competitive advantage?

Will it have a positive impact on your cost of capital (debt and/or equity)?

Is it likely to show a positive ROI?

Does it give you a new, impactful, talking point for your sales and marketing effort?

Will the program introduce you to sustainability-seeking prospective customers?

Will it have a positive impact on your staff?

Will your investors and lenders like it?

Come attend this online forum about sustainable certification

A coalition of more than 50 countries has committed to protect almost a third of the planet by 2030 to halt the destruction of the natural world and slow extinctions of wildlife.

The High Ambition Coalition (HAC) for Nature and People, which includes the UK and countries from six continents, made the pledge to protect at least 30% of the planet’s land and oceans before the One Planet summit in Paris on Monday, hosted by the French president, Emmanuel Macron.

Scientists have said human activities are driving the sixth mass extinction of life on Earth, and agricultural production, mining and pollution are threatening the healthy functioning of life-sustaining ecosystems crucial to human civilisation.

In the announcement, the HAC said protecting at least 30% of the planet for nature by the end of the decade was crucial to preventing mass extinctions of plants and animals, and ensuring the natural production of clean air and water.

The commitment is likely to be the headline target of the “Paris agreement for nature” that will be negotiated at Cop15 in Kunming, China later this year. The HAC said it hoped early commitments from countries such as Colombia, Costa Rica, Nigeria, Pakistan, Japan and Canada would ensure it formed the basis of the UN agreement.

Elizabeth Maruma Mrema, the executive secretary of the UN Convention on Biological Diversity, welcomed the pledge but cautioned: “It is one thing to commit, but quite different to deliver. But when we have committed, we must deliver. And with concerted efforts, we can collectively deliver.”

The announcement at the One Planet summit, which also saw pledges to invest billions of pounds in the Great Green Wall in Africa and the launch of a new sustainable finance charter called the Terra Carta by Prince Charles, was met with scepticism from some campaigners. Greta Thunberg tweeted: “LIVE from #OnePlanetSummit in Paris: Bla bla nature Bla bla important Bla bla ambitious Bla bla green investments…”

As part of the HAC announcement, the UK environment minister Zac Goldsmith said: “We know there is no pathway to tackling climate change that does not involve a massive increase in our efforts to protect and restore nature. So as co-host of the next Climate Cop,the UK is absolutely committed to leading the global fight against biodiversity loss and we are proud to act as co-chair of the High Ambition Coalition.

“We have an enormous opportunity at this year’s biodiversity conference in China to forge an agreement to protect at least 30% of the world’s land and ocean by 2030. I am hopeful our joint ambition will curb the global decline of the natural environment, so vital to the survival of our planet.”

However, despite support for the target from several countries, many indigenous activists have said that increasing protected areas for nature could result in land grabs and human rights violations. The announcement may also concern some developing countries who are keen for ambitious commitments on finance and sustainable development as part of the Kunming agreement, not just conservation.

Unlike its climate equivalent, the UN Convention on Biological Diversity covers three issues: the sustainable use of nature, sharing benefits from genetic resources, and conservation. The three pillars of the treaty can clash with each other and richer, developed countries have been accused of focusing too much on conservation while ignoring difficult choices on agriculture and providing finance for poorer nations to meet targets.

The HAC, currently co-chaired by France, Costa Rica and the UK, was formed in 2019 following the success of a similar climate body that spurred ambitious international action before the Paris agreement. By promoting action on biodiversity loss, it is hoped early commitments from the HAC will ensure a successful agreement for nature.

Over the last decade, the world has failed to meet a single target to stem the destruction of wildlife and life-sustaining ecosystems.

On Monday, leaders from around the world met in person and virtually at the One Planet summit in Paris to discuss the biodiversity crisis, promoting agroecology and the relationship between human health and nature. Boris Johnson, Angela Merkel and Justin Trudeau addressed the event, which also included statements fromUN secretary general, António Guterres, and the Chinese vice-premier Han Zheng .

The UK government has also committed £3bn of UK international climate finance to supporting nature and biodiversity over the next five years.

Johnson told the event: “We are destroying species and habitat at an absolutely unconscionable rate. Of all the mammals in the world, I think I am right in saying that 96% of mammals are now human being or livestock that human beings rely upon.

“That is, in my view, a disaster. That’s why the UK has pledged to protect 30% of our land surface and marine surface. Of the 11.6bn that we’ve consecrated to climate finance initiatives, we are putting £3bn to protecting nature.”

The funding was welcomed by conservation and environmental organisations, including the RSPB and Greenpeace, but there were questions about the scale of the funding and whether it came at the cost of international aid.

“Increasing funds to protect and enhance nature is critical to help secure success at the global biodiversity conference in China this year. Siphoning off cash from funds already committed to tackling the climate crisis simply isn’t enough,” said Greenpeace UK’s head of politics, Rebecca Newsom.

“This announcement raises concerns that the UK’s shrinking aid budget is being repurposed to pay for nature and biodiversity. As important as these are, the first priority of overseas aid should be the alleviation of poverty,” said Oxfam’s senior policy adviser on Climate Change, Tracy Carty.

This article was amended on 12 January 2020 to better reflect that the High Ambition Coalition (formed 2011) and the High Ambition Coalition for People and Nature (formed 2019) are separate organisations

The end of 2020 marked the moment, under the Paris Agreement’s “ratchet mechanism”, when nations were supposed to formally submit more ambitious commitments for cutting their emissions.

However, just 45 “parties” (44 countries, plus the EU’s 27 member states viewed as one bloc) met this deadline.

After a year disrupted by the Covid-19 pandemic, nations representing only around 28 per cent of global emissions registered new or updated “nationally determined contributions” (NDCs) on the UN’s official registry by the end of the year.

Some big emitters did register their NDCs in time, including the UK and EU. But major absences included the US, India and China.

Informal consultations at COP25 Madrid. Credit: Kiara Worth | IISD/ENB.

Even among the new submissions, many showed no increase in ambition since the first pledges made five years ago, or even backtracked with scaled-back proposals.

Here, Carbon Brief analyses the various new pledges and how they add up. However, one expert tells Carbon Brief that, while there was reason for hope among the new NDCs, the collective plans are still “totally off” what is required to achieve the Paris Agreement’s global warming targets.

Why were new climate pledges expected in 2020?

Every party that signed up to the Paris Agreement has to commit to a target for cutting its share of global emissions, known as its NDC, every five years.

In the run up to the COP21 climate summit in Paris, most nations had submitted intended nationally determined contributions (INDCs), which automatically became their first NDCs unless parties chose to submit updated versions.

A few countries like North Korea and Panama chose to hold off and submit their NDCs after ratifying the Paris Agreement.

According to the United Nations Framework Convention on Climate Change (UNFCCC), 190 parties, including the 27 EU member states, have now submitted first NDCs. A handful, including Iran, Iraq and Turkey have yet to do so.

Most of the pledges to reduce emissions within the NDCs were communicated as percentage reductions from a fixed baseline by a fixed year, although some, notably China and India, based theirs on cuts in “emissions intensity of GDP”. To add to the confusion, nations picked different starting points and target years.

Crucially, the initial round of INDCs was not enough to meet the climate targets set out in Paris, a point acknowledged at the time by world leaders.

Estimates suggest they would set the planet on a course for around 3C of warming, rather than the 2C or stretch target of 1.5C that nations had agreed in Paris in 2015.

Now, five years after the Paris Agreement was adopted, countries are obliged to renew and upgrade their NDCs. This is the first test of the “ratchet mechanism” embedded in the agreement, which seeks to scale up the ambition of pledges over time.

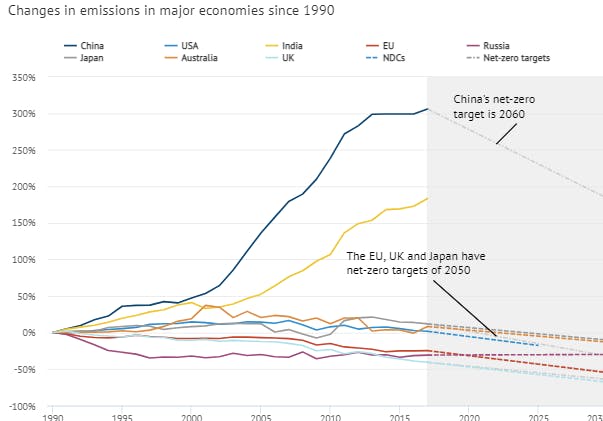

The chart below shows the progress some of the world’s major economies have made in cutting emissions from a baseline of 1990 – which is used by the EU and UK.

The coloured dotted lines indicate a linear trajectory of necessary further cuts to meet their NDC targets for 2030. China and India’s GDP-based NDCs are not shown, but the light grey line indicates the progress China, the UK and the EU must make towards their net-zero targets.

Change in greenhouse gas emissions, per cent, from 1990 for a selection of key economies, with rough pathways to NDC (coloured dotted lines) and net-zero (light grey dotted lines) targets based on a simplified and indicative linear trajectory, not actual projections of future emissions pathways. Historical emissions data includes all greenhouse gases and land use, land-use change and forestry (LULUCF), but only goes as far as 2017, which impacts the trajectory of NDC and net-zero targets. Unlike other parties, the US has not submitted a 2030 NDC yet so its pathway only goes to 2025. China and India do not have NDCs expressed as emissions percentage reductions, so their NDC pathways are not included. The EU’s net-zero trajectory is difficult to see as it follows a similar trajectory to its NDC pathway. Source: Climate Watch. Charts made by Carbon Brief using Highcharts.

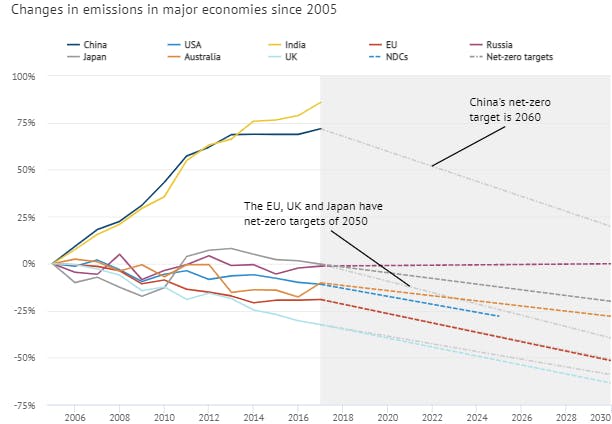

This chart, meanwhile, shows the progress some of the world’s major economies have made in cutting emissions from a baseline of 2005, which is used by the US.

Change in greenhouse gas emissions, per cent, from 2005 for a selection of key economies, with rough pathways to NDC (coloured dotted lines) and net-zero (light grey dotted lines) targets based on a simplified and indicative linear trajectory, not actual projections of future emissions pathways. Historical emissions data includes all greenhouse gases and land use, land-use change and forestry (LULUCF), but only goes as far as 2017, which impacts the trajectory of NDC and net-zero targets. Unlike other parties, the US has not submitted a 2030 NDC yet so its pathway only goes to 2025. China and India do not have NDCs expressed as emissions percentage reductions, so their NDC pathways are not included. The EU’s net-zero trajectory is difficult to see as it follows a similar trajectory to its NDC pathway. Source: Climate Watch. Charts made by Carbon Brief using Highcharts.

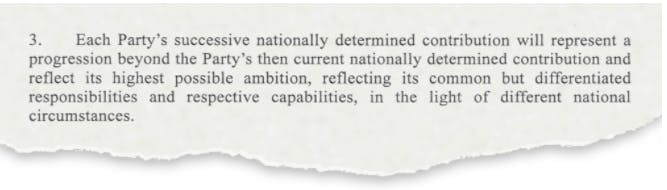

In line with the Paris Agreement, nations that only set an initial NDC covering the period up to 2025, such as the US, must now produce one that goes to 2030, and those that already contained a 2030 target must “communicate or update” their NDCs.

The agreement also states “the efforts of all parties will represent a progression over time” and will reflect the “highest possible ambition”.

However, as the text does not explicitly require new pledges to be submitted if they already run to 2030, there is room to interpret it as meaning that previous NDCs can be re-communicated. Adopting clearer language on the need for ambition was a contentious topic at COP25 in 2019.

“There is a legal dispute on what is allowed and what is not allowed, Prof Niklas Höhne from Climate Action Tracker (CAT) tells Carbon Brief, adding that nevertheless he sees it clearly:

I would argue that in the last five years, for example, renewables have become much, much cheaper than they were projected five years ago, so the situation is completely different and every country can go back and check whether they can do a little bit more.

Niklas Höhne, founder, Climate Action Tracker

Parties were initially asked in the decision text following the Paris Agreement to inform the UN of their new NDCs nine to twelve months before the COP26 climate summit in Glasgow so that the UNFCCC secretariat could prepare a synthesis report based on their contents.

Just three nations representing around 0.1 per cent of the world’s emissions met this deadline.

This “symbolic” date was ultimately delayed after the Covid-19 pandemic led to the COP’s postponement.

Instead, the UNFCCC announced it would publish an initial version of the NDC report by 28 February 2021, based on the NDCs in its registry as of 31 December 2020. The report will then be updated with any new information closer to COP26.

While some nations expressed concerns about their capacity to assemble new NDCs by the end of the year, a letter written in August 2020 by UNFCCC executive secretary Patricia Espinosa made it clear that the end-of-year deadline was still considered important.

“I strongly encourage Parties to submit their updated or new NDCs in accordance with this timeline,” she wrote.

Which nations have announced new targets?

The table below shows the nations that heeded Espinosa’s advice and made their new announcements by 31 December 2020.

The EU, Russia, Brazil, Australia, Japan, South Korea, Argentina, Mexico, Zambia and the UK are the only economies each contributing around 1 per cent or more of global emissions that have announced new targets.

However, as analysis by CAT indicates, some nations that met the deadline merely restated past commitments or made new ones that did not substantially increase ambition. (See section below.)

Many of the first countries to come forward with updated NDCs were small island states and other nations that are highly exposed to climate impacts, but contribute very little to global emissions. The Marshall Islands, for example, submitted its new NDC almost two years earlier than most other parties.

Also included in the table are nations that have indicated an intention to “enhance ambition or action in new or updated NDCs”, as recorded by the WRI’s Climate Watch resource.

This group contains an additional 82 nations, accounting for around 33per cent of total emissions.

Many of these commitments came from an announcement made at COP25 by 103 countries to “enhance ambition of their NDCs by 2020”.

China, the world’s largest emitter, remains the biggest omission from the table, although its leader Xi Jinping announced at a UN climate ambition summit in December that his nation would aim for carbon neutrality by 2060 and scale up its 2030 NDC in line with this. However, China has yet to formally register its new NDC with the UN.

China’s proposed NDC changes include a cut to the CO2 intensity of its GDP by more than 65per cent from 2005 levels, compared to its earlier target of 60-65per cent. While this marks an increase in ambition, it suggests that – in the short term and depending on assumptions about GDP growth – China’s emissions cuts will be modest. (See Carbon Brief’s analysis of China’s new 2030 pledge.)

Meanwhile, the US does not appear in the table above, although president-elect Joe Biden is expected to set out plans for a new NDC after he has taken office later this month and the US re-joins the Paris Agreement.

Other major emitters that have not come forward with new plans include India, Indonesia, Iran, Canada, Saudi Arabia and South Africa. Collectively, these six nations contribute around 17per cent of global emissions.

Do the new pledges reflect an increase in ambition?

Submission of a new NDC does not automatically mean a more ambitious commitment and commentators have pointed out that several of the plans released by large countries fall short of what is required.

At the “climate ambition summit” hosted online last month by the UN, UK and France to mark the fifth anniversary of the Paris Agreement, 45 nations came forward with enhanced NDCs.

According to Taryn Fransen, an international climate change policy expert at WRI, there has been a “mixed bag” so far, with the EU and UK in particular taking a “significant step up”.

She notes that a number of Latin American countries have also raised their ambition, including Argentina, Chile, Colombia and Peru.

Prof Niklas Höhne from CAT tells Carbon Brief that, while the situation is “much better” than he would have imagined six months ago, “it is still not sufficient”.

We have several countries that have submitted the same thing or even [gone] backwards, so there’s still a lot to do this year…What’s very clear is that we are not a little bit off we are totally off when you add all the different pledges of countries.

Niklas Höhne,founder, Climate Action Tracker

NDCs from major economies have been analysed by CAT to assess whether or not they represent an increase in ambition from previous commitments.

Lower ambition: Brazil and Mexico

Brazil has been the subject of extensive criticism for producing a new NDC that not only fails to raise ambition, but uses an accounting “trick” to make its initial pledge less ambitious.

The nation says it will cut emissions by 43per cent over the next decade compared to 2005 levels, the same as its previous proposal.

However, methodological changes in the emissions inventory since the first pledge was made mean this is now a considerably higher starting point.

The Climate Observatory, a Brazilian NGO, estimates this would mean an additional 400m tonnes of CO2e (MtCO2e) being released in 2030 compared to the original 2015 plan.

As of 2017, Brazil’s total annual emissions were around 1.4bn tonnes of CO2 (GtCO2).

The nation has also mentioned a potential 2060 net-zero goal, but said this is conditional on the payment to Brazil of $10bn per year in climate finance by other countries.

In a critique of the government’s plans, WWF says this request comes “despite [Brazil] being one of the 10 largest economies in the world”.

As a result, CAT has downgraded Brazil’s NDC from “insufficient” for meeting Paris goals to “highly insufficient”. President Jair Bolsonaro was also excluded from the recent climate ambition summit due to his nation’s insufficient plans.

Fransen says Mexico has similarly submitted a new pledge, based on a business-as-usual baseline, that is weaker than its original NDC.

“In the updated NDC they have revised those [baseline] projections upwards which of course means their achieving their target will result in higher 2030 emissions than it would have before,” she says.

The NDC has also got rid of a reference to emissions peaking in 2026.

Lacking ambition: Russia and Vietnam

Russia states in its new NDC that it “demonstrates an increasing ambition compared to earlier commitments to limit greenhouse gas emissions”.

Its previous submission from 2019 contained a commitment to cut emissions by between 25-30per cent of 1990 levels by 2030.

The new one pledges to cut emissions by 30per cent. (Russia was one of the last nations to submit a first NDC, having only ratified the Paris Agreement in October 2019.)

But the ambition of this NDC is debatable given Russia’s emissions have already fallen by more than 30per cent since 1990.

Following the end of the Soviet Union in the early 1990s and the restructuring of the economy, the nation’s emissions dropped dramatically. But, in recent years, its emissions have been growing.

“[Russia] is basically proposing a target that would be met anyway,” says Höhne. He adds that Vietnam is also using a similar strategy.

According to CAT, Vietnam is set to “vastly overachieve its updated NDC”, as the business-as-usual emissions trajectory it is based on has been “hyper-inflated”, meaning no new policies will be required to achieve it.

Same ambition: Australia, Japan and others

Australia has faced criticism for submitting a “new” NDC without a substantial change to the old one. Therefore, it has been deemed “insufficient” by CAT.

While the new NDC states that it represents a “floor on Australia’s ambition” and that the nation “is aiming to overachieve”, energy minister Angus Taylor has said there are no plans to make a more ambitious pledge in the near future.

Other nations that have similarly made no significant changes include Switzerland and Singapore.

Japan, South Korea and New Zealand, having re-submitted their original NDCs with unchanged targets, have all announced plans to reappraise their submissions in 2021 and come forward with stronger pledges.

For the two east Asian nations, this news comes after their governments revealed plans to aim for net-zero emissions by 2050, commitments that will require new shorter term targets as well.

“I think that is a good sign of the Paris Agreement working…governments feel pressured to say ‘OK we need to do more’,” says Höhne.

How much climate finance has been requested?

Every nation that has signed up to the Paris Agreement is expected to cut its emissions, but there is an expectation that poorer nations will be helped by aid – known as “climate finance” – from richer ones.

Financing climate action is, therefore, an important component of many NDCs.

Reflecting the varying levels of detail in the NDC documents, some parties have provided precise figures for their financial requirements, while others are more vague.

The table below shows explicit mentions of international climate finance requests included in the new round of NDCs, as well as plans for domestic funding. (Carbon Brief produced a similar table of requests for international funds in the first round of NDCs in 2015.)

In the latest round, a total of $373bn in international climate financing has so far been requested by developing nations. A large chunk of this is the $236bn quoted by Ethiopia.

However, as Carbon Brief stressed in its 2015 analysis of finance requests, there are important caveats to consider when looking at the total figure. For example, the types of requests can be very varied and often not directly comparable.

Some NDCs mentioned sums of money, but did not specify whether the funds they required would be sourced domestically or internationally.

Many countries that did not include specific numbers made it clear their targets depended on some level of financial support from other countries.

Nations agreed in 2009 that they would provide climate finance of $100bn a year by 2020, primarily through the UN-backed Green Climate Fund (GCF).

The GCF has often struggled to raise enough money from richer nations. The only country that makes a specific reference to providing money to the fund in the new NDCs is Monaco.

More detail on international financial requirements will likely be revealed as more NDCs emerge in the coming months.

Fransen tells Carbon Brief that a trend she has seen with the latest NDCs is that the sums being requested are “much more robust” than the previous round. “Countries have just had a lot more time to build their capacity,” she says.

This story was published with permission from Carbon Brief.

A real estate developer in Florida has unveiled what he claims is the state’s largest Tesla Solar Roof install — and it’s earned the praise of Elon Musk.

The ChoZen Retreat, an environment-focused resort on the 22,000 acre Saint Sebastian nature preserve, is graced by a staggering 44-kilowatt Solar Roof. It harnesses several times more energy than the average installation — house roofs are normally below 10 kilowatts — yet the gargantuan roof only covers around 80 percent of the resort’s energy usage.

“One of the best Tesla Solar Roof installations,” Tesla CEO Elon Musk wrote on his Twitter page Saturday.

It’s an impressive display for Tesla’s roof product, unveiled as part of a “house of the future” in October 2016. At the event, Musk explained how the tiles could pair with a Tesla Model 3 electric car and Powerwall battery to offer complete zero-emissions energy usage for a household. The solar-harvesting tiles are designed to blend in with non-solar dummy tiles, making it look like a standard roof to the untrained eye.

Tony Cho, the founder of real estate development firm Metro 1, shared a video of the Solar Roof project via his Twitter page on December 30. Watch the aerial flyover video below:

“I just installed the largest (44KW) solar roof in Florida,” Cho wrote. “Thank you [Elon Musk] for creating this game-changing product! Everyone should have one and now the 26 percent fed tax credit has just been extended!”

The video explains the installation uses nearly 800 panels to harvest DC electricity. This is channeled to inverters to convert it to AC electricity, which is then fed into Powerwall batteries. These are used to ensure the site runs from clean energy even when the Sun’s not shining. A Tesla underlay is used to protect the panels from morning dew and humidity.

ChoZen Retreat, the video claims, is the first center of its kind to receive a Tesla Solar Roof. It’s also the first home in Indian River County, Florida to receive the roof. It is the 26th home in the state of Florida.

The roof far outranks other projects done on regular houses. Amanda Tobler, one of the first to get a Solar Roof in spring 2018, told Inverse at the time that her 9.85-kilowatt system was the largest Tesla could install at that time. Her 2,000-square-foot roof consisted of around 40 percent solar tiles, the rest dummy tiles.

Tesla’s product has changed a lot since those early installs. In October 2019, Musk unveiled the third-generation tiles designed for faster and cheaper installs. While the older roofs rolled out at a slow pace, Musk said the company was aiming for 1,000 roofs per week, eventually installing a roof in just eight hours. A timelapse video in October 2020 showed the roof being installed on one house in just four days.

How much was Cho’s install?

“Not much more than a traditional roof with solar,” he wrote on Twitter.

THE INVERSE ANALYSIS — Cho’s roof is an impressive display of a product that is gradually rolling out to homes. It also acts as a symbol of how Tesla is aiming for more than just electric cars.

The actual price of the new install is unclear. Cho claims the roof cost just a bit more than a regular roof plus solar panels, but Musk claimed at the roof’s October 2019 unveiling the new tiles would cost “less than what the average roof costs plus solar panels” in “80 percent” of cases. Cho’s mega-install may be something of an outlier, perhaps understandable considering the project’s sheer scale.

But even if few customers buy the Solar Roof — you’d need to be buying a roof for the cost to make sense — it could still serve a useful purpose. At the company’s Battery Day in September 2020, Musk unveiled a plan to produce enough batteries to transition the world onto clean energy. As Musk aims to grow the energy side of the business from around seven percent to 50 percent of revenue long-term, projects like Cho’s mega-roof seem an eye-catching way to communicate how Tesla wants to transition all energy usage to clean sources.

Bonn, 11 November 2019. In the EU alone, public institutions spend EUR 2 trillion a year on procurement processes, making public procurement a major lever for achieving sustainability goals. For several years now, public-procurement legislation and regulations have increasingly included sustainability criteria. Having already been mainstreamed throughout Europe in the current EU Public Procurement Directive (2014/24/EU) issued in 2014, these criteria have been incorporated into the national legislation of the member states. Nonetheless, practical integration of sustainability criteria into public procurement processes has so far been the exception rather than the rule. Both mandatory and optional regulations need to be translated into practice.

A paradigm shift is already emerging in this regard at the international level and was also observable at the second MUPASS Dialogue Forum, which brought together public procurement experts from Germany, Europe, Latin America and Africa in Bonn in late October. These experts discussed ways of implementing a sustainable public procurement system, for instance, by incorporating sustainability criteria into e-procurement processes and making general use of sustainability standards. If there is no simple textbook approach to this topic, then experience-sharing and joint learning are the key tools for bringing about change.

In addition to a sound legal basis, there is a need for change management approaches, additional personnel and specific advice on implementation. In highly decentralised public procurement systems such as Germany’s, municipal procurement authorities require greater external support. Entities such as the Competence Center for Sustainable Procurement and the Service Agency Communities in One World already offer advisory and support services in this regard. In order to reach Germany’s 11,000 plus municipalities, the federal states need to finally join the German Government in fulfilling their responsibility to provide relevant services. It is worth taking a look at the Netherlands in this context, where central advisory institution PIANOo has successfully initiated sustainable procurement measures in the country’s municipalities (of which there are just 355) and employs over 30 staff to advise and support them. Many African nations, such as Ghana and South Africa, also run regular training campaigns for procurement officers which increasingly incorporate the topic of sustainability.

There is a need to provide training and establish new structures to equip procurement authorities and those who request and use the procured products to develop and apply sustainable procurement criteria. This has been seen in Germany and Europe and around the world, from Bremen, Berlin and Rotterdam to Tshwane in South Africa.

Communicating sustainability goals to the market can be a time-consuming process. Organising bidder dialogues, which give procurement agencies an opportunity to discuss their expectations with potential bidders, takes careful preparation and broad-based public relations work. African practitioners in particular are concerned about engaging in closer dialogue with companies due to the perceived corruption risk. However, frank exchange with the market not only provides an opportunity to strengthen sustainable procurement, but can also increase transparency regarding the procurement process.

The digitalisation of procurement is currently raising many expectations. In addition to boosting effectiveness and transparency, e-procurement could also be used to incorporate sustainability goals into the process. The city of Mainz and the Brazilian state of São Paulo, for example, are using electronic catalogues to raise buyers’ awareness of more environmentally friendly and fair alternatives within existing framework agreements. Nevertheless, new procedures alone will not ensure more effective integration of sustainability criteria into the public procurement process. When it comes to making these and other procurement instruments more sustainable, it is crucial to take account of sustainability as an integral system component in their use from the outset. The procurement agencies need corresponding support with changing their mindset on this topic.

We are currently experiencing a turning point in the world of public procurement. Consolidating long-term, strategic planning in procurement, promoting greater professionalism and introducing and piloting new procedures, such as bidder dialogues and digital processes, are all suitable ways of integrating social and environmental sustainability to a greater extent in public procurement. It is important on the way to achieving this to make the necessary resources for these change processes available, something which pays off in the form of increased efficiency and longer-term planning and facilitates both national and international dialogue between administrations. This emerging turning point is not a foregone conclusion – it must be supported and shaped.

Stoffel, Tim / Maximilian Müngersdorff

The Current Column (2019)

Bonn: German Development Institute / Deutsches Institut für Entwicklungspolitik (DIE),

The Current Column of 11 November 2019

The Commercial Bank of Ceylon was recently presented the ‘Excellent Green Commitment Award’ for the Banking Sector for 2019 by the Green Building Council of Sri Lanka (GBCSL), the country’s leading authority on implementing green concepts and green building practices.

The award was received by the Bank at the ’10th Anniversary Celebrations and Green Building Awards Ceremony 2019’ held at the Earls Regency Hotel in Kandy at which building owners, building material manufacturers and business leaders who demonstrated their commitment to environmental sustainability during 2019 were honoured. Commercial Bank was the only bank to receive this special award in the banking industry.

The award recognises Commercial Bank’s leadership in multifaceted Green initiatives encompassing lending to support eco-friendly operations, migrating customers to paperless banking, reducing consumption of non-renewable energy, water and other resources in its own operations, and support to community initiatives that help conserve habitats and the environment.

Commercial Bank financed the first commercially-viable wind power project and the first commercial-scale solar power project developed in Sri Lanka. It also continues to support projects that focus on renewable energy, energy and water efficiency, waste management, emission reductions, drip irrigation, and rain water harvesting. The Bank is also involved in the formulation of a Sustainable Banking Initiative (SBI) in the country in partnership with 18 members of the Sri Lanka Banks’ Association.

The Bank’s Green Financing is geared towards the fight against climate change, meeting the Sustainable Development Goals 7 and 12 of the United Nations Global Compact (UNGC): Affordable and Clean Energy, and Responsible Consumption and Production.

Furthermore, Commercial Bank adopts a Social and Environmental Management System (SEMS) to assess and manage social and environmental risks in a strategic and systematic manner. Procedures and work flows within the framework of SEMS ensure that the Bank’s lending is to environmentally sustainable, socially acceptable and economically viable projects.

The Bank’s ‘Green Loans’ and ‘Green Leases’ too are noteworthy, as they facilitate the purchase of energy-efficient household equipment, the installation of energy-efficient lighting for households, the purchase of hybrid or electric vehicles, solar panels and other machinery or equipment used for renewable energy, energy efficiency, emission reductions, water and waste water management and waste management. A total of Rs 5.446 Billion in Green Loan facilities was disbursed by the Bank in the period assessed for the award. These loans are expected to reduce the environmental footprint of borrowers.

Stringent measures are also in place to manage consumption and eliminate waste across the Bank’s branch network. These involve adecrease in paper usage in banking operations and the use of recycled paper, and the limiting of water consumption mainly for the purposes of drinking and sanitation.

Additionally, the Bank’s installation of solar power systems at branches, its use of waste management companies that follow international standards in disposal practices for the dispatch of e-waste and paper, initiatives to migrate customers to digital platforms, and investments in automated technology that minimise the use of paper and encourages paperless-banking are among the environment-friendly efforts initiated by the Bank.

Commercial Bank also ensures that it collaborates only with suppliers that adhere to the Bank’s sustainability standards; especially when it comes to the purchases of solar panels and air conditioners.

The Green Building Council of Sri Lanka is a consensus-based not-for-profit organisation with diverse and integrated representation from all sectors of the property industry and academia. Established in 2009 as a joint effort of the professional institutions of architects, engineers, structural engineers, town planners, quantity surveyors, university academics, construction industry leaders, environmentalists and business leaders, the organisation’s aim is to transform the Sri Lankan construction industry with green building practices and to fully adopt sustainability as the means by which the environment thrives, the economy prospers and society grows.

The only Sri Lankan Bank to be ranked among the world’s top 1000 banks for nine years consecutively, Commercial Bank operates a network of 268 branches and 865 ATMs in Sri Lanka. The Bank has won over 80 international and local awards in 2018 and 2019, and was ranked among the 10 Most Admired Companies in Sri Lanka in 2019.

Commercial Bank’s overseas operations encompass Bangladesh, where the Bank operates 19 outlets; Myanmar, where it has a Representative Office in Yangon and a Microfinance company in Nay PyiTaw; and the Maldives, where the Bank has a fully-fledged Tier I Bank with a majority stake.

Photo caption – (From left) Commercial Bank’s Junior Engineer – Premises Department Mr K. K. D. Ravindra Kamburawala and Chief Manager – Premises Department Mr Tilak Wakista with the Excellent Green Commitment Awards presented to the Bank by GBCSL.

When we hear Africa, the first thing that comes in our mind that it is the world’s second largest continent and second most-populated continent with 1.2 billion people. But it is strange that around 600 million people in Africa are living without having regular access to electricity and most of the population lives in rural areas which are hard to reach.

For these people, it would take many more years to gain access to electricity, and this entire process will require the right amount of investment. Though, business entrepreneurs and households in rural Kenya has discovered a promising solution to this problem in installation of mini-grids to meet their day-to-day demands,

Local businesses can be connected to the microgrids provided by the community, and the payments can be taken through online mobile money system which is already being used in many countries worldwide.

In the past few decades, with the significant advancement in technology and reduced production costs, solar technology has become quite inexpensive and affordable. The growing availability of solar appliances like solar fans, LED lights, solar refrigerators, TV and the other types of equipment has increased the solar energy expansion in rural areas.

Why is Africa moving towards Solar and renewable energy?

A published study Brighter Africa by McKinsey has stated that sub-Saharan Africa will utilize about 1600 terawatt of electricity by the year 2040, and it is four times of utilized electricity of the year 2010 and Similar to combined electricity of Latin America and India in 2010 (but still there are 30 % of the population who still do not have access to electricity.)

The investment required to meet this production level by 2040 is around $490 billion and $345 billion will be required for its transmission and distribution. There will rise in the share of natural gas from 6 to 45 % by the year 2040, and the expense of coal will drop from 51 % to 23%. The share of renewables will increase up to 26% which is presently around 21%.

Future Scope of Solar and Renewable Energy for Africa

Solar and wind energy has now become the most efficient way to generate energy as the life span of the coal-powered station has almost completed. By 2050, around 95 % of electricity in Africa will be generated by using renewable energy resources like solar, wind and geothermal energy.

Renewable energy is the most effective solution to the long-running shortage of electricity supply in South Africa as in Africa around two-thirds of the population which is approximately 600 million people have electricity access. With only seven countries of this continent with exceeding 50% of electricity rates, electricity access is the main reason behind the development. It is essential to power telecommunication, water supply, healthcare, and educational services.

With the potential of generating 10 terawatts of solar energy, 1 gigawatt of geothermal energy and 1300 gigawatts of wind power, renewable energy will be the future of Africa. It will eliminate the requirements of fossil fuels which has a negative impact on the environment as well as society. African governments, as well as the private sector, are now finding cheaper and smarter ways to produce the energy and tackle the electricity deficit in the continent.

Most of the experts agree that Africa requires to increase its electricity production by using renewable sources like wind, predominantly solar and hydroelectric. Africa is the continent of a growing private market for renewable energy ventures which results in the increased number of investors who are investing in the development of technologies that can lead to sustainable and clean energy generation.

Energy market of various countries in Africa is experiencing a structural transformation which is in the direction of a more economically integration of renewable energies. The rapid rollout of wind and solar energy in some of the African Countries depicts that “renewable plays an essential role in the overall energy mix Africa.”

According to the Solar Magazine interview with Benjamin Attia ( Wood Mackenzie Power & RenewablesAnalyst), stated that Wood Mackenzie had a collaborative partnership with Energy 4 impact(Non-profit organization). They seek to decrease poverty by accelerating energy access. They are providing bsiness, financing, and technical advice to off-grid energy businesses working in sub-Saharan Africa.

Facts related to Solar and Renewable Energy Implementation in Africa?

Rising off-grid solar investment

In early December, Government of UK stated that they will invest another ₤100 million through the REPP (Renewable Energy Performance Platform) in various projects. So, it boosts the growth of the renewable energy sector of Sub Saharan Africa. This fund was made in 2015 for helping the project developers to overcome the financial problems.

Wind, hydroelectric, spanning solar, biomass and geothermal power generation, the REPP program is funding 18 renewable energy projects in different countries of Sub-Saharan Africa which includes Tanzania, Kenya, Nigeria, and Burundi – as per the news update.

The new funding of €100 million will manage the finance of many projects and programs based on renewable energy in Sub-Saharan Africa for the upcoming five years as per the UK government. Moreover, REPP is an integral part of the UK commitment to internationally invest about €5.8 billion regarding climate finance by 2020.

Geographic and downstream off-grid solar expansion

Sub Saharan off-grid solar companies continuously raising financial sources for expanding geographically and to enhance the range of their off-grid electronic products. Also:

During Dec 2011, Off-Grid Electric or Zola Electric had stated that it has acquired about USD 32.5 million credit facility, so that they can finance and manage their activities in Tanzania within the five years.

D.light was established in 2007, it works towards providing solar power to 62 countries and around 88 million people according to the management. The products and services offered by company extend to include the portable solar lanterns which double as the LED lighting, flat-screen TV, mobile phone rechargers and the small home appliances.

The D.light has raised around US$100 million in the past two years in equity and debt financing. Even, some of the initial investors of D.light took profit of the latest investment funding and make their exit.

Final Verdict

As the power sector sub-Saharan Africa facing various challenges but still there is a real push for change. Like Sustainable Energy program of UN assisting private sector activity in various parts of the value chain. Even, the region holds the ability to lead the sector development to the new level. And the Success will drive the economic growth of the continent and improve the lives of millions of people. Also, supports in increasing electricity supply over various industry and providing millions of jobs around the continent.

Here’s the question for oil industry investors. Can oil companies scale up clean energy enterprises to replace business lost from a decline in fossil fuel revenues? Some of the oil companies put up a brave front as they boast of their decarbonization plans. Others ignore the question. But at the end of the day— and this is the takeaway— we don’t think they will replace lost fossil related income by massively investing in windmills and solar power. Here’s why. It’s a simple matter of risk and return. Investors accept lower returns when they make low risk investments (regulated utilities for example). Except for nuclear power, non-fossil fuel investments are lower in risk than fossil fuel investments. Energy exploration by its nature entails risk of financial loss. There is no such thing as a dry hole in the wind or solar industries. That is why renewable industries can attract new capital while offering investors steady but lower returns.

If oil managements do decide to enter the renewables business in a big way, as opposed to mere greenwashing, they may have to accept a lower rate of profitability. If they don’t, they will have a hard time obtaining business.

The inherently lower business risk of renewables distinguishes it from the oil business. Renewables do not require massive investments taking decades to fully develop in inhospitable and unfriendly places like the ocean floor. Their projects are bankable as soon as they have contracts signed. They do not compete against state controlled entities with few capital or environmental constraints. They can contract for a steady flow of revenues and pay regular dividends. Environmental accidents do not have multi-billion dollar consequences. Okay, weather can affect performance, but on balance performance averages out. In brief, renewable energy projects can be characterized as relatively small, or modular, with short duration of construction (planning takes longer), predictable revenues with limited foreign exposure. Low risk, low return. This profile doesn’t have the investment attributes of the oil business at all.

Maybe, though, the oil industry could find a suitable new opportunity in nuclear energy. From our perspective some of its investment attributes are similar: projects with long lead times, large concentration of capital in one project, relatively low risk of catastrophic accident but high risk that any accident will be really bad, ongoing need for negotiation with and cooperation from the government authorities. Big oil’s scale gives it an edge. New nuclear projects are too big nowadays for most energy companies.

And unlike renewables, if the nuclear builder negotiates aggressively it can extract an appropriately high return that reflects the risk. New nuclear construction is one business that most resembles the oil industry in terms of risk, possible return and scale. The obvious catch is that not many for-profit businesses want to get involved with new nuclear construction and operation for good reasons, all of which are well known to our readers.

But with better construction management, research to develop a new generation of reactors and permanent waste storage, who knows? A new generation of nuclear power plants might emerge just when the oil companies need to find big replacements for lost income. This is still a possibility. But if we assume that commercialization of new nuclear technology is at least a decade away that still leaves a big hole in prospective capital budgets. What to do in the meantime other than drill for oil?

In short, we don’t expect the oil industry to grow in any meaningful way with wind turbines and large solar arrays. The demand for capital in the renewable industry is high but the returns may not be high enough for oil investors.

Maybe the oil industry has confused its end market with its business strengths. It seems to see itself as purveyor of energy on a mass scale. Okay, but that market will become crowded with purveyors of new energy products who work for less. Perhaps, instead, the oil industry’s strength is not its customer base but rather its skill as a financier, developer and operator of risky resources on a massive scale, akin to the giant mining and trading combines, but with more technological skill.

Oil and electricity are both commodities but with very different margin structures. Perhaps the oil industry would be better served by investing in potentially high margin commodity businesses like cobalt or rare earth metals, for example, without which no batteries can be made. Or, it could invest in resources or capital intensive processes that will be required for decarbonization.

In short, replace oil profits with windmill and solar profits? Other people can do it as well. Oil companies will need to do something big, and maybe as daring as drilling for oil in the old days. How about, for instance, a process to remove carbon dioxide from the air and turning it into chemicals and fuels on a vast scale? They need to start thinking on a bigger scale. Otherwise, why bother?

By Leonard Hyman and William Tilles for Oilprice.com

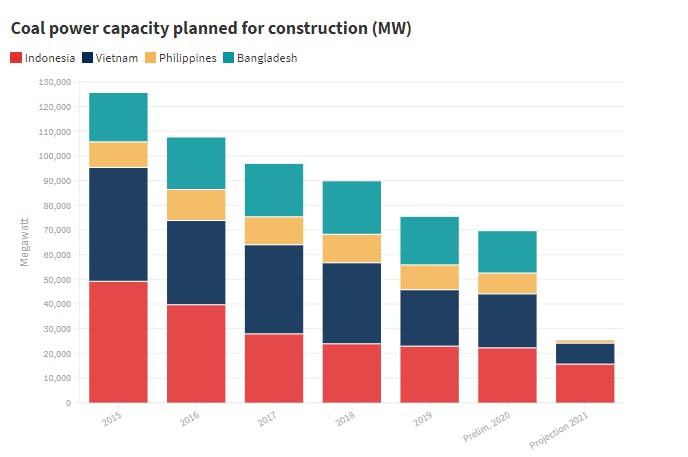

Long seen as a critical emerging market for coal power, South and Southeast Asian countries radically reconsidered their commitment to it last year in the face of new economic realities following the spread of coronavirus.

According to a new analysis from Global Energy Monitor (GEM), four of the region’s largest emerging economies— Bangladesh, Indonesia, the Philippines and Vietnam—may have cancelled nearly 45 gigawatts (GW) of coal power in 2020, equivalent to the total installed capacity of Germany.

Prospects for a revival of coal development plans in 2021 have also been limited by announcements from major coal financiers in South Korea and Japan of new restrictions on coal power investments beyond their borders.

Analysts have for years warned that coal power expansion plans in several countries in South and Southeast Asia risked overcapacity in the sector, wasted capital and asset stranding—not to mention greenhouse gas emissions and environmental costs. The year 2020 may prove to be when the regions’ coal power expansion plans were finally re-evaluated in the face of the pressing need for climate action and the reality of declining low-carbon technology costs.

Falling one by one

Perhaps the most dramatic development in Asia’s energy sector last year was the summer flurry of coal power plant cancellations and postponements. It started in Bangladesh in June when Nasrul Hamid, Minister for Power, Energy and Mineral Resources, unexpectedly announced that the government was planning to “review” all but three of the country’s under-development coal plants, capping coal power capacity at 5GW. Suddenly, planned coal plants totalling 23GW were in doubt. By November, Bangladeshi media were reporting that the plan to scrap most of the country’s planned coal was awaiting approval from the prime minister.

A month later, details of Vietnam’s draft Power Development Plan, which is due to come into force next year, became public. The draft plan proposed cancelling seven coal plants and postponing six others until the 2030s, by which point it is highly unlikely they will go ahead. The 13 plants represent almost half of Vietnam’s planned coal power development.

Then, in November, the Philippines’ Department of Energy proposed a moratorium on new coal power plants which, according to analysis by GEM, could lead to 9.6GW of cancellations. And, in December, on the fifth anniversary of the Paris Agreement, Pakistan’s Imran Khan announced that the country would not construct any new coal power plants, though the real-world impact of this grandiose announcement has been questioned.

Adding in proposed project cancellations in Indonesia, GEM estimates that the coal power pipeline in South and Southeast Asia’s four major emerging economies may have dropped by as much as 62GW in 2020. That leaves just 25GW under development, an 80 per cent decline from just five years ago. Exact figures for cancelled and remaining plants will depend on how last year’s flurry of announcements is manifested in specific policies.

Source: Global Energy Monitor (GEM)

The financial drought continues

One contributing factor to the wave of coal power cancellations and moratoriums around South and Southeast Asia last year was the decline in finance. Banks faced growing public pressure to identify and manage the climate and biodiversity risks associated with coal power development and respond to the climate crisis by committing resources to renewables. A recent report from Greenpeace Japan estimates that Southeast Asia’s renewable energy market could be worth up to US$205 billion over the next 10 years.

In Japan, 2020 saw banks Mizuho, Sumitomo Mitsui, and Mitsubishi UFJ Financial Group announce restrictions on coal power investments. In Korea, state financial institutions Korea Export-Import Bank and KSURE both stepped away from involvement in coal power projects, while Samsung corporation and the state-owned Korea Electric Power Corporation pledged no further investments in overseas coal projects.

The Japanese government also committed “in principle” to limit investments in overseas coal power plants, declaring that such investments would be contingent on the use of ultra-supercritical technology and the host country having a decarbonisation strategy. There have also been strong moves within the Korean parliament this year to ban Korean financing of coal power overseas, with progressive MPs from the ruling Democratic Party proposing related bills on four occasions.

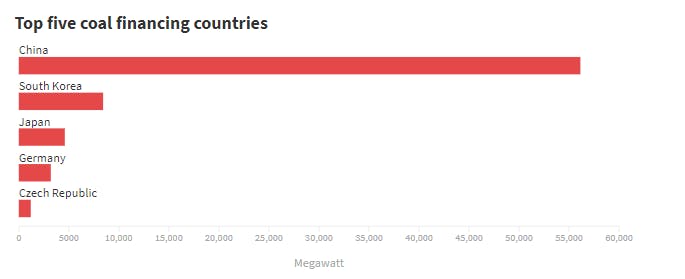

The wave of announcements comes on the back of Singapore’s three major banks announcing an end to coal power financing in 2019. This leaves Chinese banks increasingly the “lender of last resort” to coal power projects around Asia. According to the Global Coal Public Finance Tracker, Chinese banks have provided finance to a total of 53GW worth of under construction or currently operating coal power, far more than the 21GW propped up by the second biggest financier in overseas coal, Japanese banks.

Source: Global coal public finance tracker • Note: The data covers all projects under development since 2013, including currently proposed projects, which have received or are likely to receive public finance.

All eyes on China’s policymakers

But movement may be on the horizon in China too. At the beginning of December, a report released by the BRI International Green Development Coalition and supported by the Ministry of Ecology and Environment detailed how the Chinese government could establish a “classification mechanism” of overseas project types based on their impacts on local pollution, climate change and biodiversity. The mechanism labels coal power and coal mining as “red”, meaning that involvement of Chinese actors in such projects would be off-limits. Eyes are now on policymakers to adopt the report’s suggestions.

The growing number of national pledges to reach carbon net-zero has arguably given impetus toward “greening” the Belt and Road Initiative. Though China’s new 2060 net-zero goal is targeted at the domestic economy, numerous voices are calling for the expansion of the development target to overseas investments.

While these dizzying developments in Asian energy are certainly welcome news, “king coal” is still clinging on in several places. Countries such as Vietnam and Indonesia, despite their large-scale cancellations, are still pursuing the construction of significant quantities of coal power, while Cambodia has announced new coal power projects, backed by Chinese finance and construction. Meanwhile, despite its welcome net-zero announcement, China is still building new coal-fired power plants at an alarming rate at home.

Asia’s journey away from coal will be a long one but in 2020 many countries at least picked up the pace.

Recycling closes the loop for a circular economy, but the more complicated the packaging design, the lower the chance of it being recycled. Could mono-material packaging be the answer to this problem?

‘Circular economy’ has become the buzzword for businesses around the world, regardless of industry. Oftentimes, the phrase is merely used for marketing purposes, with little attention paid to its concepts and principles.

There are numerous players involved in the lifecycle of one product. From raw materials suppliers and logistics companies, to manufacturers, distributors, consumers, and disposal, it may not be sufficient when only one of the players upstream creates a ‘circular product’ without involving the other players downstream to ensure that the loop can truly be closed.

Over the centuries, the human-environment relationship has grown from a circular one to a linear one. In the past, what our ancestors used to take from nature was returned to nature at the end of its life.

No material is as difficult to differentiate as plastic.

From a material scientist’s perspective, civilisation developed along with newly synthesised materials that allowed technology to flourish—materials that nature is unable to assimilate in a short period of time. Nevertheless, learning to be better stewards of materials can drive our economy back to a circular one.

For the packaging industry, the answer may lie in mono-materials.

Packaging serves a necessary function—protecting or preserving the product it contains. The material chosen for the packaging has to satisfy this basic functionality. But as products get increasingly sophisticated, more functionalities of packaging are needed and a single material may not be able to satisfy all of the requirements.

Laminations, coatings and additives went into the material formulation to achieve the packaging solution. The need for labels to print the necessary product information and branding further complicated the design. This is how a simple packaging purely used to contain a product can become a concoction of differing materials.

Recycling cannot deal with mixed materials, even for plastics.

No material is as difficult to differentiate as plastic. A transparent plastic can be polyethylene terephthalate (PET), polyvinyl chloride (PVC) or even general-purpose polystyrene (PS).

But these plastics cannot be mechanically recycled together and have to be separated, if not the quality of the recycled PET (which has a higher recycled value) will be downgraded or even contaminated beyond reusability.

The process of mining iron comes from extracting iron ores since iron does not exist as a pure element on earth. This requires energy input to purify the ores to obtain pure iron before it can be further used in the manufacturing of products.

The reverse engineering of products (such as recycling) into individual materials follows the same process. Recycling could be an energy-intensive activity, but it helps to close the loop for a circular economy in packaging products.

However, the more complicated a packaging design, the more effort is needed.

Unfortunately, this segregation often comes from human intervention in developing countries before the actual recycling can take place. If packaging consists of only one material, these preliminary steps can be avoided. The pathway to recycling will also be shorter and more efficient.

For the multi-layered materials that cannot be separated, either simply because it is not economically viable or not intervenable manually, the easiest method would be to take the inseparable materials and downcycle them into a composite particle board.

The only way to know if this mixture of inseparable materials is durable or even toxic is through testing it, but the composite particle board is thereafter rendered non-recyclable.

Is it possible to standardise the transparent plastic type to use for takeaways?

When it comes to determining which plastics to use for packaging, retailers are simply spoiled for choice. But when it comes to service packaging (e.g. takeaway containers), do we really need to look beyond PET and PP?

In the resin code, 7 refers to ‘others’, yet this one number encompasses many different types of plastics, and even biodegradable plastics are currently listed under ‘7’.

To determine if the plastic is recyclable or not, a consumer must know what the resin code represents, and which types of plastic can be collected—which is dependent on the local recycling infrastructure. Such in-depth knowledge may fly over the face of most consumers.

Thus, standardising which mono-material to use for a certain type of packaging—especially those with low functionality such as single-use packaging—may be the key to ensure a truly circular economy.

Plastics have great flexibility when it comes to engineering the material into the required packaging properties. Yet it is the same flexibility that results in the proliferation of plastic types that goes beyond the 7 resin identification codes.

While certain industries like automobiles or electronics would benefit from advanced plastics, comparatively, packaging for everyday items does not require the same level of complexity.

With a thorough understanding of the recycling process and infrastructure, much can be done by the packaging design engineers to mindfully create packaging for ease of recycling.