Australia’s Great Barrier Reef suffered its most extensive coral bleaching event in March, with scientists fearing the coral recovers less each time after the third bleaching in five years.

February 2020 was the hottest month on record since records began in 1900, Professor Terry Hughes, Director of the ARC Centre of Excellence for Coral Reef Studies at James Cook University, told Reuters Newsagency.

“We saw record-breaking temperatures all along the length of the Great Barrier Reef, there wasn’t a cool portion in the north, or a cool portion in the south this time around,” Professor Hughes said. “The whole Barrier Reef was hot so the bleaching we have seen this year is the most extensive so far.”

Professor Hughes added that he was now almost certain that the Reef was not going to recover to what it looked like even five years ago, not to mention 30 years ago. If the global warming trends continued the Great Barrier Reef would be destroyed, he said.

“We will have some sort of tropical ecosystem, but it won’t look like coral reef, there might be more seaweed, more sponges, a lot less coral, but it will be a very different ecosystem.”

The Great Barrier Reef, covering 348,000 square kilometres was UNESCO world heritage listed in 1981 as the most extensive and spectacular coral reef ecosystem on the planet, according to the UNESCO website.

Water is the lifeblood of humanity. With it, communities thrive. But, when the supply and demand of fresh water are misaligned, the delicate environmental, social, and financial ecosystems on which we all rely are at risk. Climate change, demographic shifts, and explosive economic growth all exacerbate existing water issues.

However, hope is not lost. Businesses can play a leading role in mitigating the water issue to limit not just their own risk but also the risk of all stakeholders relying on these systems. This can be accomplished by directing action through three spheres of influence: direct operations, supply chain, and wider basin health.

Water today

Water is as important to the world’s economy as oil or data. Though most of the planet is covered in water, more than 97 percent of it is salt water. Fresh water accounts for the rest, although most of it is frozen in glaciers, leaving less than 1 percent of the world’s water available to support human and ecological processes. Every year, we withdraw 4.3 trillion cubic meters of fresh water from the planet’s water basins. We use it in agriculture (which accounts for 70 percent of the withdrawals), industry (19 percent), and households (11 percent).

These percentages vary widely across the globe. In the United States, industrial usage (37 percent) is almost as high as agricultural (40 percent); in India, on the other hand, agriculture claims 90 percent of water withdrawals, while only 2 percent is put to work for industry. China’s withdrawals are 65 percent agriculture, 22 percent industrial, and 13 percent for household use. Considering that some of the agricultural usage is directed toward industry—for example, half of the production of maize, which is one of the top five global crops by total acreage and water consumption, is used for producing ethanol—the figures may understate how critical water is to business.

All industries rely on water in some way. A company’s water footprint can be seen in four key areas of its value chain: raw materials, suppliers, direct operations, and product use. Consider, for example, a T-shirt across its value chain—raw materials (cotton), suppliers (cotton-to-fabric processer), direct operations (final manufacturing, shipping, and retail), and product use (washing the shirt at home). Food and beverage companies use water a

s an ingredient in the products they sell, of course, but they also use it to irrigate, rinse, and clean crops, and to feed livestock. Metals and mining companies need water for dust control, drilling, and slurry when transporting products. In the tech industry, suppliers require ultrapure water for certain manufacturing processes, and data centers require water for cooling. Forest-products companies rely on water for making pulp and paper. Apparel companies rely on water to grow raw materials and wash garments. Even insurance companies are affected by water through claims related to water, such as crop-production insurance. Water’s uses and effects are as varied as business itself.

The availability of fresh water also varies greatly by location. The majority of the world’s fresh water is divided among 410 named basins, which are areas of land where all water that falls or flows through that region ultimately ends at a single source. These include the Huang He, Nile, Colorado River, Indus, and many others. Of these 410 named basins, almost a quarter (90) are considered “high stressed” (meaning that their ratio of total annual withdrawals to total available annual supply exceeds 40 percent). These 90 highly stressed basins account for just 13 percent of the total area of named water basins but account for 51 percent of withdrawals (Exhibit 1). About half are located in three countries with enormous water needs and high economic activity: China, India, and the United States.

The water crisis is here, and it’s getting worse

Water risk is not a worry to be addressed in some nebulous future. The supply of fresh water has been steadily decreasing while demand has been steadily rising. In the 20th century, the world’s population quadrupled—but water use increased sixfold. The strain is already apparent. In 2018, in the midst of a severe drought, Cape Town, South Africa, came close to experiencing a so-called Day Zero, where the city would have literally run out of water. To avoid that peril, the city government put quotas on agricultural, business, and domestic usage. The government also got lucky: rain replenished its basin just in time. All in all, the drought drove at least 5.9 billion rand (approximately $400 million) in economic losses across the Western Cape.

In 2018, South Africa’s Western Cape experienced its worst drought in decades.

This event, and others like it, are just a taste of what’s to come. As McKinsey’s 2009 report Charting our water future: Economic frameworks to inform decision-making made clear, climate change, population growth, and changing consumer habits are increasing water stress for many regions. The recent McKinsey Global Institute report Climate risk and response: Physical hazards and socioeconomic impacts notes that many of the world’s basins could see a supply decline of around 10 percent by 2030 and up to 25 percent by 2050. By 2050, according to UN estimates, one in four people may live in a country affected by chronic shortages of fresh water. The World Bank estimates that the crisis could slow GDP by 6 percent in some countries by 2050 as well.

Water stress is a risk multiplier. Alone, it is a powerful risk with the potential to upend socioeconomic and ecological systems. When compounded with other risks, such as those related to food and energy systems, politics, and infrastructure, it becomes detrimental.

The clear and increasing business risk

Two-thirds of businesses have substantial risk in direct operations or in their value chain. As water stress grows, they will experience that risk in four forms: physical, regulatory, reputational, and stakeholder.

Physical risks can be critical and costly. In some locations, key water sources may be inaccessible or unfit for use. A primary physical risk is having too little water, which can be a costly problem. A 2015 drought in Brazil drove up General Motors’ water costs there by $2.1 million, and its electricity costs rose an additional $5.9 million.

By 2050, one in four people may live in a country affected by chronic shortages of fresh water.

As the crisis worsens, companies may find themselves increasingly beholden to the whims of government regulators. When Chinese regulators mandated in 2015 that papermakers cut water consumption by 10 percent, Chenming Group, one of the top ten players in the global paper industry and the leading player in the Chinese market, responded by upgrading its assembly line with advanced equipment that reduced daily water consumption by 45 percent. In 2017, the state government of Kerala, India, facing a severe drought, restricted PepsiCo’s groundwater consumption by 75 percent.

A company’s pro-environment reputation is becoming increasingly critical. A 2018 Nielsen survey found that 81 percent of global customers say it is important for companies to improve the environment.1 Consumers are voting with their dollars for companies that align with these principles. The same survey found that 73 percent of customers would change their purchasing habits to reduce environmental impact. In the age of single-tweet public-relations crises, the best defense is getting ahead of issues before they strike.

Stakeholder risk is rapidly growing as more companies and influential bodies become aware of the other types of business risk. These significant players are able to exert outsize influence on other businesses to nudge them toward practices that are consistent with their own sustainability and business ethos. BlackRock CEO Larry Fink cited water risk in his 2020 letter to CEOs, stating, “What happens to inflation, and in turn interest rates, if the cost of food climbs from drought and flooding?” BlackRock, which has nearly $7 trillion in assets under management, was a founding member of the Task Force on Climate-related Financial Disclosures (TCFD) and is engaging with the companies it invests in to ensure that they follow these guidelines. Moreover, BlackRock is working internally to continually improve the standards of its own reporting in this domain as well. In addition to BlackRock, more than 600 other investment firms with $69 trillion in total assets under management now urge their companies to report on water-related risks and act to mitigate them. (For more, see “‘Bring the problem forward’: Larry Fink on climate risk.”)

How businesses can tackle the problem

The water issue is the reverse of the carbon problem; the cause is global, but its manifestation is highly spatial and can be addressed in a concentrated way. Not all basins have equal priority. In fact, several basins have water withdrawals that are well within sustainable limits. Rather than tackling water use across every geography, a more efficient route is for companies to understand how they are interacting with basins that are projected to become water stressed and focus efforts there. Apple, for example, anchors its water stewardship policies by mapping its global water use against regions with heightened water risk. As a result, it focuses its efforts on three regions accounting for 52 percent of its total water use: Maiden, North Carolina; Mesa, Arizona; and Santa Clara Valley, California.

There are three spheres of influence that companies can affect to help mitigate water stress: direct operations, supply chain, and wider basin health. Some companies are already taking action in all three areas.

Direct operations

Within their four walls, companies have several levers they can use to reduce water stress. They can implement water measurement and reporting practices, even including water use in relevant company key performance indicators (KPIs). They can aggressively identify and eliminate water leaks in their operations and introduce new technologies that reduce water stress.

In 2010, Ford set a goal of using 30 percent less water per car by 2014. It reached that goal through a combination of new KPIs and operational improvements. The introduction of internal water metering alone drove conservation behaviors to the department level and helped save around $5 million worldwide. A dry-paint-spray system eliminated water from the car-painting process, and a new lubricant that replaced water in the manufacturing process saved about 280,000 gallons per production line.

The water issue is the reverse of the carbon problem; the cause is global, but its manifestation is highly spatial and can be addressed in a concentrated way.

Colgate-Palmolive partnered with a water-technology company to meet its sustainability goals for a plant located in a water-scarce basin in Mexico. Its processes require a significant amount of water to ensure proper sanitation for the toothpaste, deodorant, and soap products produced. The new solutions were able to reduce the plant’s water use by 1.8 million gallons annually while also significantly reducing the amount of time required for cleaning and sanitizing.

Supply chain

Companies can further reduce water stress by using their influence to ensure that their suppliers and their suppliers’ suppliers are equally rigorous about their own contributions to water stress. There are three critical levers to pull: reducing energy use and shifting to renewables, setting supplier standards, and sending water-expert teams to help key suppliers identify and implement efficient water-usage solutions.

Water is required to both extract many energy sources and generate energy through steam-powered turbines. The reduction of energy consumption and the market shift toward renewable sources has the dual effect of lowering greenhouse-gas emissions and reducing water withdrawals. With the transition to a more decarbonized world, new energy-investment decisions can consider water benefits alongside carbon, cost, reliability, and other lenses. The production and use of fossil fuels requires up to four times more water than the production of renewables. If the future energy mix of the planet remains the same as it is now, withdrawals from water basins for energy can grow by 25 percent by 2040. On the other hand, switching 75 percent of fossil-fuel consumption to renewables by that time, per individual countries’ Paris Agreement targets, can reduce the water footprint of energy by 47 percent (Exhibit 2).

Companies can also set reporting standards for suppliers. In 2014, Levi Strauss launched a Recycle & Reuse compliance program, which requires that each supplier meet certain limits; use a blend of at least 20 percent recycled water in its facility processing, landscaping, cooling, and plumbing; and provide flow-meter data that tracks the amount of recycled water used on Levi Strauss products.

Nike has successfully implemented a water-supplier initiative, which the company refers to as the Minimum Water Program. Teams work closely with the company’s largest materials suppliers and others to ensure good water practices by offering their own expertise to assist their suppliers. The program has been a success—in 2019, Nike achieved its initial goal of reducing fresh water used in textile dyeing by 20 percent, 18 months ahead of schedule.

Wider basin health

Some businesses may choose to go further by using their influence in partnerships that promote water resilience.

During the United Nations’ 2012 Conference on Sustainable Development, 45 of the world’s largest companies united to advocate for governments to implement sensible water policies. The companies (including Bayer, Coca-Cola, GlaxoSmithKline, Merck, and Nestlé) signed a special communiqué demanding that governments raise the price of water to a fair and appropriate price. The companies committed to ongoing lobbying to support water-positive policies, such as a fair market price for water. Without price increases, water users do not have feedback mechanisms that incentivize conservation and the development of new technologies to cut usage.

Another significant initiative is the Water Resilience Coalition, a creation of the UN Global Compact’s CEO Water Mandate. Launched in March 2020, it is built around a water-resilience pledge that binds signatory companies to a set of water goals to be addressed by collective action in water-stressed basins.

As with other key components of climate change, the time has come to address the water crisis head-on. Businesses have a key role to play.

The authors wish to thank Jonathan Glustein for his valuable content, analysis, and strategic contributions. In addition, the authors wish to thank Elaine Almeida, Maria Bernier, Katie Chen, Andrei Dan, Eduard Danalache, Annabel Farr, Philipp Hühne, Nico Mohr, Dickon Pinner, Laura Poloni, Martha Pulnicki, Rahim Surani, and Michael Zhang for their support.

A new series – the New Nature Economy reports – is being launched to make the business case for safeguarding nature.

The first, Nature Risk Rising, explains why nature-related risks have direct relevance for business through their impact and dependency on nature.

Here are five key lessons from that first report.

At the World Economic Forum’s Annual Meeting in Davos in January this year, there was unprecedented interest in and commitment to fighting the climate and nature emergencies facing humanity. Although the world’s 7.6 billion people represent just 0.01% of all living things by weight, humanity has already caused the loss of 83% of all wild mammals and half of all plants. Supporting the concept of stakeholder capitalism, leading CEOs, government leaders and heads of civil society organizations came together in the Swiss Alps to galvanize support for an integrated nature action agenda across the issues of climate, biodiversity, forests, oceans and sustainable development.

Despite increasing attention on the topic of nature loss, there is still limited understanding on how nature loss can be material to businesses and what the private sector can do to address this challenge. The World Economic Forum is launching a series of New Nature Economy (NNE) reports in 2020, making a business and economic case for safeguarding nature. Nature Risk Rising, the first of the NNE series, aims to show how nature-related risks are material to business and why they must be urgently mainstreamed in risk-management strategies.

1. Economic growth has come at a heavy cost to natural systems

The economic growth model of the 19th and 20th centuries has brought remarkable development and prosperity. Globally, we produce more food and energy than ever before. The human population has doubled, the global economy has expanded four-fold and more than a billion people have been lifted out of extreme poverty.

However, we have caused great harm to the planet. Three-quarters of ice-free land and 66% of the marine environment have been altered and 1 million species are at the risk of extinction in the coming decades, mostly due to human activities.

2. Five direct drivers are responsible for 90% of nature loss

Five direct drivers of change in nature have accounted for over 90% of nature loss in the past 50 years. Namely, land-and-sea-use change, natural resource exploitation, climate change, pollution and invasive alien species. These five drivers ultimately stem from a combination of production and consumption patterns, population dynamics and other human activities.

There is often a dissonance between economics and earth system science. While present economic frameworks see nature as an externality, nothing could be further from the truth. The global economy is embedded in Earth’s broader ecosystems and is dependent upon them.

When focused on measuring progress against the single indicator of gross domestic product (GDP), we risk failing to recognize and prevent the loss of our ecological foundations.

3. Nature loss is often hidden

Nature is often hidden or incorrectly priced in supply chains, blurring the link between nature loss and the bottom line. There are three ways in which the loss of nature creates risks for businesses:

i. Dependence of business on nature: Businesses depend directly on nature for their operations, supply chain performance, real estate asset values, physical security and business continuity. Our research shows that $44 trillion of economic value generation – over half the world’s total GDP – is moderately or highly dependent on nature and its services, and is therefore exposed to risks from nature loss. Together, the three largest sectors (construction, agriculture, and food and beverages) that are highly dependent on nature generate close to $8 trillion of gross value-added (GVA). This is roughly twice the size of the German economy.

ii. Fallout of business impacts on nature: The direct and indirect impacts of business activities on nature loss could trigger negative consequences, such as losing customers or entire markets, costly legal action and adverse regulatory changes. Consumers and investors are becoming increasingly aware of the environmental damage caused by industries and are demanding action. Companies that stay at the forefront of this shift in consumer consciousness and preferences stand to benefit.

iii. Impacts of nature loss on society: When nature loss aggravates the disruption of the society in which businesses operate, this can in turn create physical and market risks. For instance, the degradation and loss of natural systems can affect health outcomes. The onset of infectious diseases has been connected to ecosystem disturbances, including the strong links between deforestation and outbreaks of animal-transmitted diseases such as Ebola and the Zika virus.

Five direct drivers of nature loss have accelerated since 1970 Image: Nature Risk Rising report

4. A risks framework for nature

As the global community works towards transitioning to a nature-positive economy, an urgent reframing of the financial materiality of nature risks is required. The climate change agenda leveraged the Task Force on Climate-related Financial Disclosures (TCFD) framework to tackle this issue. Over 870 organizations – including companies with a combined market cap of over $9.2 trillion and financial institutions responsible for assets of nearly $118 trillion – have signed up to support the TCFD. A similar initiative – that draws lessons from the TCFD and which is backed by public and private stakeholders – is now needed for nature.

5. Business as champions for nature

As we are facing an unprecedented planetary emergency, businesses have an important role to innovate and advance solutions for a nature-positive economy and society. Some economies have shown how nature and business can work hand in hand. Costa Rica, for one, has in the last three decades stopped tropical deforestation, doubled its forest cover and reached near 100% renewable electric energy while GDP per capita has tripled. By realizing how nature-loss is material to their operations and growth models, businesses can and must be a key part of the solution. As the trend for greater transparency and accountability continues, costs are likely to rise for businesses which have not begun to include nature at the core of their enterprise operations. The World Economic Forum along with key partners and constituents will be furthering a business for nature mobilization to halt biodiversity loss and invest in nature over the coming years. The next steps are to identify the areas where strategic transformation of current business models can contribute most to halting and reversing nature loss, and the ways to finance this transition.

Please reach out to [email protected] if you want to learn more about the New Nature Economy report series and engage in the process.

Akanksha Khatri, Head, Nature and Biodiversity Initiative, World Economic Forum

The views expressed in this article are those of the author alone and not the World Economic Forum.

Climate change is a very real and serious threat to society. Extreme weather events such as heatwaves and flooding are becoming more commonplace and severe, leaving communities to deal with often devastating humanitarian and economic costs.

In the past 12 months, global protests have brought millions of young people to the streets to voice their opinions, with the result that both policy-makers and businesses are beginning to sit up and take notice. And a report by a UK environmental non-profit showed that the world’s largest 500 companies could potentially face $1 trillion of financial risks in the short term due to climate change impacts such as higher operating costs, asset write-offs and falls in demand.

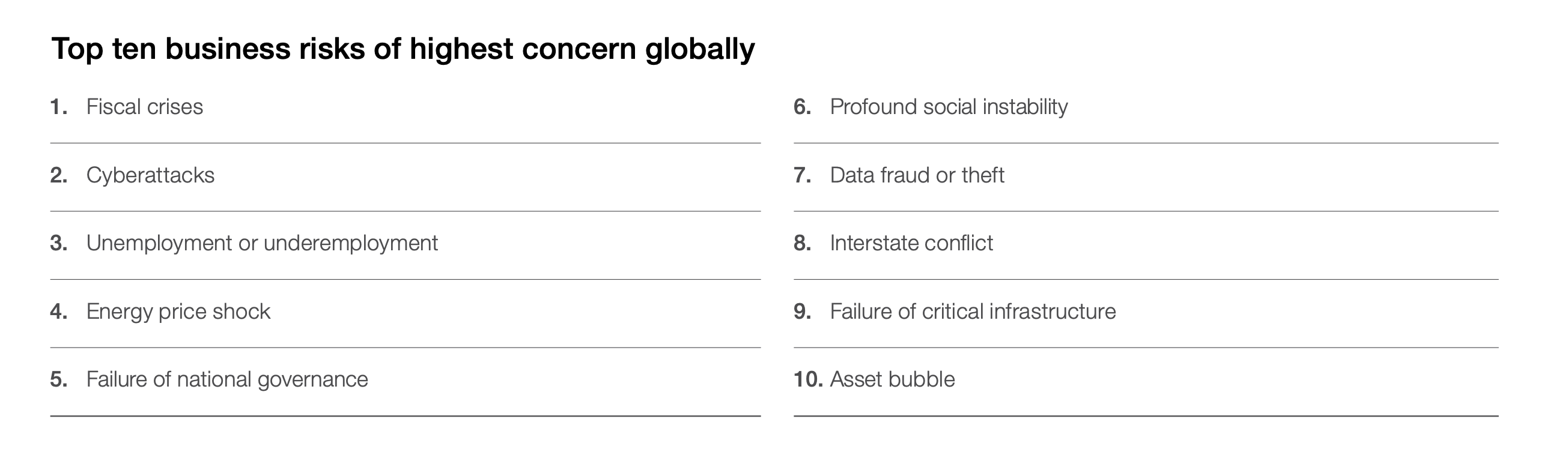

This is why, while reading the results of the World Economic Forum’s 2019 Regional Risks for Doing Business report, which is based on a survey of around 13,000 European business leaders, I was surprised to see that climate change did not appear anywhere in the top-10 risks. For me, it is the biggest existential risk for doing business in Europe – and companies need to act now to be prepared.

Unfortunately, we are not on track to meet the Paris Agreement targets. Businesses urgently need to understand where and how their operations and supply chains are vulnerable to the physical risks of climate change. Equally important is that companies assess their transition risks so that their business models not only remain relevant in a lower-carbon future, but they can seize the opportunities that will be presented.

What are the risks identified for Europe by the report?

Cyberattacks are the top threat in Europe, according to the report. The digital world continues to evolve rapidly; more and more devices are connected to the internet and attackers are getting more organized, meaning the threat from external cyberattacks is always increasing.

It’s important that customers trust the companies they do business with not to just provide them with the products and services they need, but to do so in a way that is responsible, ethical and protects their personal information.

What’s not on this list is as important as what is Image: World Economic Forum 2019 Regional Risks for Doing Business report

This means businesses must continuously invest in their cybersecurity capabilities and should allocate significant resources to proposition development and artificial intelligence. Doing so allows firms to better serve their customers and protect them against constantly evolving cyber-risks.

Turning towards macroeconomic and geopolitical risks, Europe is experiencing the twin effects of a natural slowdown in the economic cycle and a political move to the right. Unfortunately, one feeds the other: weak growth tends to result in a shift to the political right and more inward-looking economies. Factors like Brexit and the US-China trade war only serve to increase the chances of a market sell-off and to heighten volatility across the region.

“(Climate change) is the biggest existential risk for doing business in Europe”

In such a scenario, it is likely that central banks will further loosen interest rates and increase asset purchases, driving prices higher, inflating today’s asset bubble further and causing discontent among those who feel savers are being penalized.

Companies with a strong balance sheet, a global/local business model and well-diversified portfolios will be better-placed to navigate these headwinds and be there for their customers when needed. Moving from a reactive to a preventative role will become increasingly important.

Economic, geopolitical and cyber-risks undoubtedly pose an immediate threat to doing business in Europe. However, we all need to acknowledge that climate change is an existential risk to the world – and that includes how we do business. It needs to be at the forefront of decisions, because – if left ignored – the damage will be extensive and irreversible.

Alison Martin, CEO EMEA and Bank Distribution, Zurich Insurance Group

The views expressed in this article are those of the author alone and not the World Economic Forum.

water also varies greatly by location. The majority of the world’s fresh water is divided among 410 named basins, which are areas of land where all water that falls or flows through that region ultimately ends at a single source. These include the Huang He, Nile, Colorado River, Indus, and many others. Of these 410 named basins, almost a quarter (90) are considered “high stressed” (meaning that their ratio of total annual withdrawals to total available annual supply exceeds 40 percent). These 90 highly stressed basins account for just 13 percent of the total area of named water basins but account for 51 percent of withdrawals (Exhibit 1). About half are located in three countries with enormous water needs and high economic activity: China, India, and the United States.

water also varies greatly by location. The majority of the world’s fresh water is divided among 410 named basins, which are areas of land where all water that falls or flows through that region ultimately ends at a single source. These include the Huang He, Nile, Colorado River, Indus, and many others. Of these 410 named basins, almost a quarter (90) are considered “high stressed” (meaning that their ratio of total annual withdrawals to total available annual supply exceeds 40 percent). These 90 highly stressed basins account for just 13 percent of the total area of named water basins but account for 51 percent of withdrawals (Exhibit 1). About half are located in three countries with enormous water needs and high economic activity: China, India, and the United States.